10 Proven Ways to Invest in Annuities for Retirement Income

Ways to Invest in Annuities: Investing in annuities can be an excellent way to secure a steady stream of income during retirement. An annuity is a financial product that you purchase from an insurance company, which then provides you with periodic payments for a specific duration or even for life. Annuities offer several benefits, including tax-deferred growth, lifetime income, and protection against outliving your savings. However, with so many types of annuities available, it can be challenging to determine which one is right for you. In this blog post, we’ll explore the various ways to invest in annuities and help you make an informed decision.

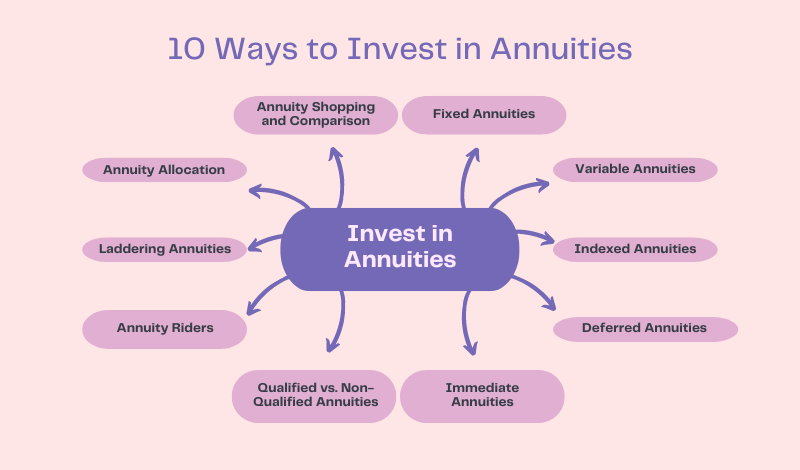

1. Fixed Annuities:

Ways to Invest in Annuities: Fixed annuities are the simplest and most straightforward type of annuity. With a fixed annuity, you make an upfront payment (or a series of payments) to an insurance company, and in return, the company guarantees you a fixed rate of return on your investment for a specified period, typically ranging from 5 to 20 years. The interest rate is determined at the time of purchase and remains unchanged throughout the contract term.

Fixed annuities are ideal for risk-averse investors who prioritize the preservation of their principal investment and a guaranteed stream of income. However, it’s important to note that fixed annuities typically offer lower returns compared to other investment options, such as stocks or mutual funds, due to their lower risk profile.

2. Variable Annuities:

Ways to Invest in Annuities: Variable annuities are more complex and offer the potential for higher returns compared to fixed annuities. With a variable annuity, your premiums are invested in subaccounts, which are similar to mutual funds but are managed by the insurance company. These subaccounts invest in various asset classes, including stocks, bonds, and money market instruments.

The value of your variable annuity fluctuates based on the performance of the underlying subaccounts. If the investments perform well, your annuity’s value will increase. Conversely, if the investments underperform, your annuity’s value will decrease.

Variable annuities offer the potential for higher returns but also carry a higher level of risk. They are more suitable for investors with a longer investment horizon and a higher risk tolerance.

3. Indexed Annuities:

Ways to Invest in Annuities: Indexed annuities, also known as equity-indexed annuities or fixed-indexed annuities, offer a unique blend of features from both fixed and variable annuities. With an indexed annuity, your principal investment is protected from market downturns, similar to a fixed annuity. However, your potential returns are tied to the performance of a specific market index, such as the S&P 500 or the Dow Jones Industrial Average.

The way indexed annuities work is that the insurance company credits your account with a portion of the index’s gains, up to a predetermined cap or participation rate. This means that your returns are limited but also protected from market losses.

Indexed annuities can be a good choice for investors seeking moderate growth potential while still maintaining some level of principal protection.

4. Deferred Annuities:

Ways to Invest in Annuities: Deferred annuities are annuities where the payments are delayed until a future date, typically retirement. During the accumulation phase, your premiums are invested, and the value of your annuity grows tax-deferred. This means you don’t have to pay taxes on the investment gains until you start receiving payments, which can be a significant advantage for long-term investors.

There are two main types of deferred annuities:

– Deferred Fixed Annuities: These are similar to traditional fixed annuities, but the payout phase is delayed until a future date.

– Deferred Variable Annuities: These are variable annuities where the payments are deferred until a later date, allowing for tax-deferred growth during the accumulation phase.

Deferred annuities can be an excellent way to build up a retirement nest egg while taking advantage of tax-deferred growth.

5. Immediate Annuities:

Ways to Invest in Annuities: Immediate annuities, also known as income annuities or payout annuities, are designed to provide you with a stream of income payments right away. With an immediate annuity, you make a lump-sum payment to the insurance company, and in return, the company begins making periodic payments to you, usually within a year of purchase.

Immediate annuities can be a good choice for retirees who need to generate income immediately or for individuals who have received a lump sum of money, such as an inheritance or a pension payout, and want to convert it into a steady stream of income.

There are several types of immediate annuities, including:

– Single-Life Annuities: These provide income payments for the remainder of your life.

– Joint-Life Annuities: These provide income payments for the lives of two individuals, typically spouses.

– Period-Certain Annuities: These provide income payments for a specified period, regardless of whether the annuitant(s) are still alive.

6. Qualified vs. Non-Qualified Annuities:

Ways to Invest in Annuities: Annuities can be further classified as qualified or non-qualified, based on the type of account used to fund the annuity.

– Qualified Annuities: These are annuities funded with pre-tax dollars from a qualified retirement account, such as an IRA or a 401(k). The money in a qualified annuity grows tax-deferred, and you’ll pay taxes on the income payments when you receive them in retirement.

– Non-Qualified Annuities: These are annuities funded with after-tax dollars from non-retirement accounts. While the money in a non-qualified annuity still grows tax-deferred, you’ll only pay taxes on the gains when you receive income payments, not on the principal amount you originally invested.

The choice between a qualified or non-qualified annuity will depend on your individual circumstances and retirement planning goals.

7. Annuity Riders:

Ways to Invest in Annuities: Many insurance companies offer optional riders or add-ons that can enhance the features and benefits of an annuity. Some common annuity riders include:

– Guaranteed Minimum Income Benefit (GMIB): This rider guarantees a minimum level of income payments, regardless of the performance of the underlying investments.

– Guaranteed Minimum Withdrawal Benefit (GMWB): This rider allows you to withdraw a guaranteed minimum amount from your annuity each year, even if the account value has been depleted.

– Guaranteed Minimum Death Benefit (GMDB): This rider ensures that your beneficiaries will receive a minimum death benefit amount, even if the annuity’s account value has declined.

Riders can provide additional protection and flexibility, but they typically come with additional costs, which can reduce your overall returns.

8. Laddering Annuities:

Ways to Invest in Annuities, Laddering annuities is a strategy that involves purchasing multiple annuities with different start dates and terms. This approach can help you manage your income stream and mitigate the risk of locking in a low interest rate for an extended period.

For example, you could purchase a 5-year fixed annuity, followed by a 7-year fixed annuity a year later, and then a 10-year fixed annuity the following year. As each annuity matures, you can reinvest the proceeds into a new annuity at the current interest rates, allowing you to take advantage of potentially higher rates over time.

Laddering annuities can be a more complex strategy, but it can provide greater flexibility and potential for higher returns in a changing interest rate environment.

9. Annuity Allocation:

Ways to Invest in Annuities, Another way to invest in annuities is through an annuity allocation strategy. This approach involves dividing your retirement portfolio among different types of annuities and other investments, such as stocks, bonds, and mutual funds.

For example, you could allocate a portion of your portfolio to a fixed annuity for a guaranteed income stream, another portion to a variable annuity for potential growth, and the remaining portion to other investments based on your risk tolerance and investment goals.

Annuity allocation can help you diversify your retirement portfolio and balance various risks and returns. However, it’s essential to carefully consider your overall asset allocation and ensure that your investment mix aligns with your financial objectives and risk profile.

10. Annuity Shopping and Comparison:

Ways to Invest in Annuities: When investing in annuities, it’s crucial to shop around and compare offerings from different insurance companies. Annuity rates, fees, and contract terms can vary significantly among providers, and even small differences can have a substantial impact on your long-term returns and income stream.

Some factors to consider when comparing annuities include:

– Interest rates or crediting rates

– Fees and expenses (e.g., surrender charges, mortality and expense fees)

– Contract terms and provisions

– Financial strength and ratings of the insurance company

– Rider options and costs

It’s also important to work with a qualified financial advisor or annuity specialist who can help you understand the complexities of annuities and guide you through the selection process.

Conclusion: Ways to Invest in Annuities

Ways to Invest in Annuities: Investing in annuities can be a valuable strategy for securing a steady stream of income during retirement, but navigating the different types and features can be complex. From fixed annuities that offer guaranteed returns to variable annuities with growth potential, each option comes with its own set of pros and cons.

Ways to Invest in Annuities, Ultimately, the right annuity choice for you will depend on your financial goals, risk tolerance, and overall retirement plan. Some investors may prefer the simplicity and security of a fixed annuity, while others may be willing to take on more risk for the potential of higher returns with a variable or indexed annuity.

Ways to Invest in Annuities, Strategies like laddering annuities or allocating a portion of your portfolio to different types of annuities can also help you diversify your retirement income sources and manage risk. Additionally, considering optional riders, such as income guarantees or death benefits, can provide added protection and flexibility, albeit at an additional cost.

Ways to Invest in Annuities, As you explore your annuity options, it’s crucial to do your due diligence, compare offerings from multiple providers, and carefully evaluate the fees, terms, and financial strength of each company. Working with a qualified financial advisor or annuity specialist can also help ensure that you make an informed decision that aligns with your unique circumstances and long-term goals.

Ways to Invest in Annuities, Investing in annuities is a significant financial commitment, but for many retirees, the guaranteed lifetime income and peace of mind they provide can be invaluable. By understanding the various ways to invest in annuities and carefully weighing your options, you can position yourself for a more secure and comfortable retirement.