Decoding 5 Different Types of Credit Scores: A Comprehensive Guide

In today’s financial landscape, credit scores play a pivotal role in determining an individual’s creditworthiness. These numerical representations of your credit history can significantly impact your ability to obtain loans, credit cards, mortgages, and even employment opportunities. However, not all credit scores are created equal. There are 5 different types of credit scores, each serving a specific purpose and calculated using different methodologies. In this comprehensive article, we’ll explore the 5 different types of credit scores and their significance in the world of personal finance.

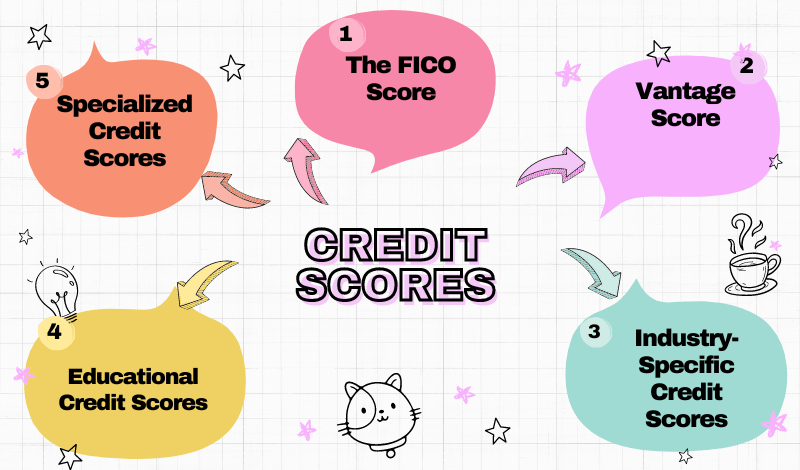

1. The FICO Score: The Industry Standard

When it comes to the 5 different types of credit scores, the FICO score is widely recognized as the industry standard. Developed by the Fair Isaac Corporation, FICO scores range from 300 to 850, with higher scores indicating a lower credit risk for lenders. This type of credit score is one of the 5 different types of credit scores and is used by most lenders, including banks, credit card issuers, and mortgage companies, to evaluate an individual’s creditworthiness.

FICO scores are calculated based on various factors, including payment history, amounts owed, length of credit history, types of credit used, and new credit inquiries. While FICO scores are widely used and one of the 5 different types of credit scores, it’s important to note that different lenders may have their own customized scoring models or criteria for evaluating creditworthiness when considering the 5 different types of credit scores.

2. VantageScore: An Alternative Credit Scoring Model

The VantageScore is another of the 5 different types of credit scores and an alternative credit scoring model developed by the three major credit bureaus: Experian, Equifax, and TransUnion. Like FICO scores, which are also one of the 5 different types of credit scores, VantageScores range from 300 to 850, with higher scores indicating a lower credit risk. This scoring model aims to provide a more consistent and predictive approach to credit scoring across all three credit bureaus when evaluating the 5 different types of credit scores.

VantageScores are calculated using similar factors as FICO scores, which are among the 5 different types of credit scores, such as payment history, credit utilization, and credit age. However, the specific algorithms and weightings of these factors may differ from those used by FICO when considering the 5 different types of credit scores. VantageScores have gained popularity among lenders, particularly those seeking an alternative to FICO scores or catering to consumers with limited credit histories, and are one of the 5 different types of credit scores used by lenders.

3. Industry-Specific Credit Scores

In addition to the more widely recognized credit scores like FICO and VantageScore, which are among the 5 different types of credit scores, there are also industry-specific credit scores tailored to particular lending sectors. These specialized scores, also counted among the 5 different types of credit scores, are designed to assess credit risk for specific types of loans or financial products when evaluating the 5 different types of credit scores.

1. Auto Credit Scores: Lenders in the automobile industry often use specialized credit scores, such as the FICO Auto Score or the Experian Automotive Credit Score, to evaluate an individual’s creditworthiness for auto loans or leases.

2. Mortgage Credit Scores: When applying for a mortgage, lenders may utilize credit scores specifically designed for the mortgage industry, such as the FICO Mortgage Score or the VantageScore for Mortgage Lenders. These scores aim to better predict the risk of default on mortgage loans.

3. Credit Card Credit Scores: Credit card issuers may use credit scores tailored to the credit card industry, like the FICO Bankcard Score or the VantageScore for Credit Cards, to assess an individual’s creditworthiness for new credit card accounts or credit limit increases.

These industry-specific credit scores, which are part of the 5 different types of credit scores, are calculated using similar factors as the more general credit scores like FICO and VantageScore, but may place different weights on certain factors based on the specific lending industry’s needs and risk models when evaluating the 5 different types of credit scores.

4. Educational Credit Scores

Educational credit scores, one of the 5 different types of credit scores, are designed to help individuals understand their credit standing and identify areas for improvement. These scores, which are part of the 5 different types of credit scores, are typically provided by credit bureaus or credit monitoring services and are not used by lenders for decision-making purposes when considering the 5 different types of credit scores.

Educational credit scores, one of the 5 different types of credit scores, often include additional information and analysis beyond the numerical score, such as detailed explanations of the factors impacting the score, personalized recommendations for improving credit, and credit monitoring tools. While not used for lending decisions when considering the 5 different types of credit scores, educational credit scores can be valuable resources for individuals seeking to build or maintain a strong credit profile among the 5 different types of credit scores.

5. Specialized Credit Scores

In addition to the types of credit scores mentioned above, such as FICO, VantageScore, industry-specific scores, and educational scores, which are all part of the 5 different types of credit scores, there are also specialized credit scores that cater to specific segments of the population or address unique financial scenarios when considering the 5 different types of credit scores. Examples include:

1. Bankruptcy Credit Scores: These scores are tailored to individuals who have recently filed for bankruptcy and are aimed at assessing their creditworthiness as they rebuild their credit.

2. Thin-File Credit Scores: These scores are designed for individuals with limited credit histories or those who are new to credit, helping lenders evaluate their creditworthiness based on alternative data sources.

3. Business Credit Scores: These scores are used by lenders and creditors to assess the creditworthiness of businesses, rather than individuals, and are based on factors such as payment history, outstanding debt, and industry risk.

While these specialized credit scores may not be as widely used as the more common types like FICO and VantageScore, which are part of the 5 different types of credit scores, they can play a crucial role in providing access to credit for individuals or businesses in unique financial circumstances when evaluating the 5 different types of credit scores.

Conclusion

Understanding the different types of credit scores is essential for navigating the complex world of personal finance and creditworthiness. From the industry-standard FICO score to alternative models like VantageScore, industry-specific scores, educational scores, and specialized scores, each type serves a distinct purpose and caters to various lending scenarios.

It’s important to remember that while credit scores are valuable tools for lenders, they are not the sole determinant of creditworthiness. Factors such as income, employment history, and overall financial responsibility also play a significant role in lending decisions.

By staying informed about the various types of credit scores and their implications, individuals can take proactive steps to build and maintain a strong credit profile, increasing their chances of securing favorable terms for loans, credit cards, mortgages, and other financial products.