Why is it Important to Have an Emergency Fund?

Introduction:

Emergencies can strike at any time, and they often come with unexpected financial burdens. From medical emergencies to job loss, car repairs, or home maintenance issues, these unexpected events can put a significant strain on your finances. This is where having an emergency fund, or a sum of money set aside specifically to Build an Emergency Fund for unforeseen expenses, comes into play. An emergency fund is a sum of money set aside specifically for unforeseen expenses, providing a financial safety net when life throws you a curveball. In this comprehensive guide, we’ll explore the importance of having an emergency fund and the strategies to build and maintain one effectively.

Understanding the Concept of an Emergency Fund:

An emergency fund, or a separate savings account dedicated solely to Build an Emergency Fund to cover unexpected expenses that would otherwise disrupt your regular budget or financial plan, is designed to provide a buffer against financial shocks, preventing you from going into debt or dipping into your retirement savings or other long-term investments.

The primary purpose of an emergency fund is to:

– Cover unexpected medical bills

– Pay for essential repairs (e.g., car, home)

– Tide you over during periods of job loss or reduced income

– Handle emergency travel expenses

– Address other unforeseen circumstances that require immediate financial resources

Why is an Emergency Fund Crucial?

Having an emergency fund is crucial for several reasons:

1. Protects Your Financial Stability

Unexpected expenses can easily derail your financial plans if you don’t have a dedicated fund to Build an Emergency Fund and cover them. Without an emergency fund, you may be forced to rely on high-interest credit cards, take out loans, or tap into your retirement savings, which can have long-term consequences for your financial well-being.

2. Reduces Financial Stress

Knowing that you have a safety net in place by taking steps to Build an Emergency Fund can provide peace of mind and alleviate the stress that often accompanies financial emergencies. With an emergency fund, you can tackle unexpected expenses without the added burden of worrying about how to come up with the money.

3. Prevents Debt Accumulation

When you don’t have an emergency fund or haven’t taken steps to Build an Emergency Fund, you may be tempted to turn to credit cards or loans to cover unexpected expenses. This can lead to a vicious cycle of debt accumulation, with interest charges compounding the problem. An emergency fund allows you to pay for emergencies without incurring additional debt.

4. Preserves Your Retirement Savings

Dipping into your retirement accounts, such as 401(k)s or IRAs, to cover emergencies can have significant consequences. Not only do you risk depleting your nest egg, but you may also face penalties and taxes for early withdrawals. An emergency fund, or taking steps to Build an Emergency Fund, safeguards your retirement savings and ensures that your long-term financial goals remain on track.

Determining the Appropriate Size of Your Emergency Fund:

The size of your emergency fund when you Build an Emergency Fund will depend on your individual circumstances, such as your income, expenses, and potential risks. Generally, financial experts recommend having enough savings to cover three to six months’ worth of living expenses. However, some factors may suggest a larger or smaller emergency fund:

1. Your Job Stability

If you have a stable job with a low risk of job loss, you may be able to get away with a smaller emergency fund (e.g., three months’ worth of expenses) when you Build an Emergency Fund. However, if your job is more volatile or you’re self-employed, it’s advisable to have a larger emergency fund (e.g., six to nine months’ worth of expenses) to cover potential income gaps.

2. Your Family Size and Dependents

Larger families with more dependents may need a larger emergency fund to account for additional expenses, such as childcare or healthcare costs, when they Build an Emergency Fund. Single individuals or couples without children may be able to get by with a smaller emergency fund.

3. Your Income and Expenses

If you have a high income and relatively low expenses, you may be able to build up your emergency fund more quickly and have a larger cushion when you Build an Emergency Fund. On the other hand, if your income is lower and expenses are higher, you may need to start with a smaller emergency fund and gradually build it up over time.

4. Your Risk Tolerance

Some people may feel more comfortable with a larger emergency fund, even if their circumstances suggest a smaller one, when they Build an Emergency Fund. Your risk tolerance and peace of mind should also factor into the size of your emergency fund.

Building Your Emergency Fund:

Creating an emergency fund doesn’t happen overnight. It requires disciplined saving and a solid strategy to Build an Emergency Fund. Here are some tips for building your emergency fund:

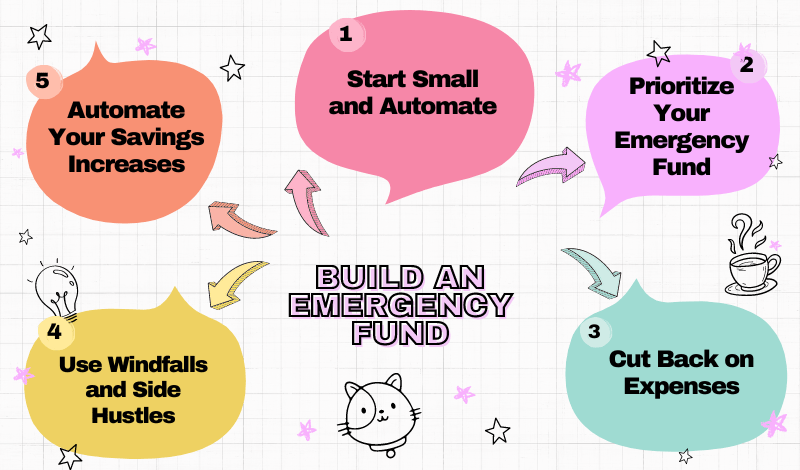

1. Start Small and Automate

If you’re starting from scratch to Build an Emergency Fund, don’t be discouraged. Begin by setting aside a small amount each month, even if it’s just $25 or $50. Automate your savings by setting up automatic transfers from your checking account to a dedicated savings account. This way, you’ll be less tempted to spend the money, and your emergency fund will grow steadily over time.

2. Prioritize Your Emergency Fund

When you receive a raise, bonus, or windfall (e.g., tax refund), prioritize contributing a portion of that money to Build an Emergency Fund. This will help you build it up more quickly.

3. Cut Back on Expenses

Examine your monthly expenses and identify areas where you can cut back, even temporarily. Reduce discretionary spending, such as dining out, entertainment, or subscription services, and redirect those funds towards Building an Emergency Fund.

4. Use Windfalls and Side Hustles

If you receive unexpected income, such as a tax refund, inheritance, or money from a side hustle, allocate a portion (or all) of it to Build an Emergency Fund.

5. Automate Your Savings Increases

As your income grows, consider automating an increase in your emergency fund contributions. Build an Emergency Fund: For example, you could set up your savings to increase by 1% or 2% each time you receive a raise.

Maintaining and Replenishing Your Emergency Fund:

Once you’ve built up your emergency fund, it’s essential to maintain it and replenish it after using it for an emergency: Build an Emergency Fund.

1. Keep Your Emergency Fund Separate

Keep your emergency fund in a separate, easily accessible account, such as a high-yield savings account or a money market account. Build an Emergency Fund. This will prevent you from accidentally spending it on non-emergencies and will also make it easier to track your progress.

2. Replenish After Use

After using your emergency fund, make it a priority to replenish it as soon as possible. Build an Emergency Fund. This will ensure that you’re prepared for the next unexpected expense.

3. Periodically Review and Adjust

As your life circumstances change (e.g., job change, marriage, children), review your emergency fund periodically and adjust the amount as needed to ensure it still meets your needs. Build an Emergency Fund.

Where to Keep Your Emergency Fund:

When it comes to where to keep your emergency fund, there are several options to consider: Build an Emergency Fund:

1. High-Yield Savings Account

A high-yield savings account is a popular choice for emergency funds. Build an Emergency Fund. These accounts typically offer higher interest rates than traditional savings accounts, allowing your money to grow slowly while still being easily accessible when needed.

2. Money Market Account

Money market accounts are another option for emergency funds. Build an Emergency Fund. These accounts often have slightly higher interest rates than savings accounts and may offer check-writing privileges or debit card access, making it easier to access your funds in an emergency.

3. Certificate of Deposit (CD)

CDs can also be used for emergency funds, but they typically have penalties for early withdrawals, which can limit your access to the funds. Build an Emergency Fund. If you choose to use CDs, consider using a ladder strategy, where you open multiple CDs with staggered maturity dates, ensuring that some of your funds are always accessible without penalties.

4. Combination of Accounts

Some people choose to split their emergency fund across multiple accounts, such as a high-yield savings account for immediate access and a CD or money market account for a portion of the funds to earn slightly higher interest rates. Build an Emergency Fund.

Alternatives to Traditional Emergency Funds:

While a dedicated emergency fund is the recommended approach, there are alternative strategies that some people use: Build an Emergency Fund:

1. Home Equity Line of Credit (HELOC)

A HELOC allows you to borrow against the equity in your home. While this can provide access to funds in an emergency, it also puts your home at risk if you’re unable to repay the loan. Build an Emergency Fund.

2. Roth IRA Contributions

Contributions to a Roth IRA can be withdrawn penalty-free in an emergency, as long as you don’t touch the earnings. However, this strategy should be used with caution, as it can potentially derail your retirement savings goals. Build an Emergency Fund.

3. Borrowing from Family or Friends

In some cases, people may consider borrowing from family or friends in an emergency. While this can be a viable option, it’s important to have a clear repayment plan and consider the potential strain on personal relationships. Build an Emergency Fund.

It’s important to note that these alternatives come with their own risks and limitations, and a dedicated emergency fund remains the recommended approach for most people. Build an Emergency Fund.

Conclusion: Build an Emergency Fund

Having an emergency fund is an essential component of a solid financial foundation. It provides a safety net against life’s unexpected curveballs, protecting your financial stability, reducing stress, preventing debt accumulation, and safeguarding your retirement savings.

While building an emergency fund requires discipline and commitment, the strategies outlined in this guide can help you get started and gradually build a financial cushion that aligns with your individual circumstances and risk tolerance.

Remember, an emergency fund is not a one-time effort; it requires ongoing maintenance and replenishment after each use. By regularly reviewing and adjusting your emergency fund, you can ensure that it continues to meet your evolving needs and provides the peace of mind that comes with knowing you’re prepared for whatever life throws your way.

Investing in an emergency fund is an investment in your financial security and overall well-being. It’s a proactive step towards financial resilience and a testament to your commitment to responsible money management. So, start building your emergency fund today, and take control of your financial future.