What is the Difference Between a Traditional and Online Bank

Introduction

In today’s digitalized world, the way we handle our finances has undergone a significant transformation. While traditional brick-and-mortar banks have been the norm for decades, online banks have emerged as a convenient and cost-effective alternative. As consumers, it’s essential to understand the 6 key differences between a traditional and online bank to make an informed decision that aligns with our financial needs and preferences. In this article, we’ll explore the distinctions between traditional and online banks, highlighting their respective advantages and drawbacks.

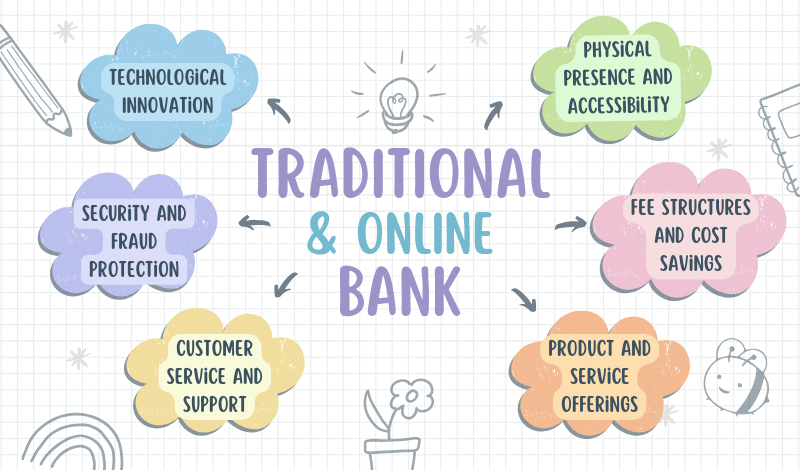

1. Physical Presence and Accessibility

One of the most apparent differences between traditional and online banks lies in their physical presence and accessibility. 6 Difference Between a Traditional and Online Bank, Traditional banks maintain a network of physical branches and ATMs, providing face-to-face interactions with bank personnel and tangible access to banking services. Customers can visit a branch to open accounts, apply for loans, or seek personalized financial advice from banking professionals.

Difference Between a Traditional and Online Bank, online banks operate entirely through digital channels, without any physical branches or ATMs. Customers can access their accounts, perform transactions, and manage their finances through a website or mobile app. This model eliminates the need for physical visits, making banking services accessible from anywhere with an internet connection.

2. Fee Structures and Cost Savings

One of the primary advantages of online banks is their lower overhead costs, which often translate into lower fees and better interest rates for customers. By operating without the expenses associated with maintaining physical branches and employing a large workforce, online banks can pass these cost savings on to their customers in the form of higher interest rates on savings accounts and lower fees for various services.

Traditional banks, on the other hand, typically have higher operating costs due to their physical infrastructure and personnel requirements. As a result, they may charge higher fees for services like account maintenance, ATM usage, and wire transfers. However, some traditional banks offer promotional rates or fee waivers to attract and retain customers.

3. Product and Service Offerings

Both traditional and online banks offer a range of products and services, including checking and savings accounts, credit cards, loans, and investment options. However, the breadth and depth of these offerings may vary between the two banking models.

6 Difference Between a Traditional and Online Bank, Traditional banks often have a more comprehensive suite of products and services, including specialized offerings like wealth management, business banking, and investment advisory services. They may also have established relationships with third-party providers, such as insurance companies and investment firms, enabling them to offer a wider range of financial solutions.

Online banks, while generally offering the core banking products, may have a more limited selection of services, particularly in areas that require physical interactions or specialized expertise. However, many online banks are continuously expanding their offerings to meet the evolving needs of their customers.

4. Customer Service and Support

Difference Between a Traditional and Online Bank, Customer service and support are crucial aspects of any banking experience. Traditional banks typically provide multiple channels for customer support, including in-person interactions at branch locations, dedicated phone lines, and online chat or email support. This personal touch can be valuable for customers who prefer face-to-face interactions or require assistance with complex financial matters.

Online banks, on the other hand, primarily rely on digital channels for customer support, such as phone lines, email, and online chat. While these channels can be efficient and convenient, some customers may prefer the personal touch of face-to-face interactions, especially for more complex financial transactions or inquiries.

5. Security and Fraud Protection

Both traditional and online banks prioritize the security of their customers’ financial information and transactions. However, their approaches to security may differ.

Difference Between a Traditional and Online Bank, Traditional banks often employ a combination of physical security measures, such as surveillance systems and armed guards, as well as digital security protocols like encryption and multi-factor authentication. They may also have dedicated fraud prevention teams to monitor and respond to potential threats.

Online banks, lacking a physical presence, rely heavily on digital security measures, including advanced encryption techniques, multi-factor authentication, and sophisticated fraud detection algorithms. They may also employ third-party security providers to ensure the highest levels of protection for their customers’ data and transactions.

6. Technological Innovation

Difference Between a Traditional and Online Bank, In the rapidly evolving digital landscape, online banks tend to be at the forefront of technological innovation. As their primary mode of operation is digital, they are often quicker to adopt new technologies and implement advanced features, such as mobile banking apps, biometric authentication, and integration with personal finance management tools.

Traditional banks, while investing in digital transformation initiatives, may face challenges in keeping pace with technological advancements due to their legacy systems and established processes. However, many traditional banks have recognized the importance of digital innovation and are actively partnering with fintech companies or developing their own digital solutions to remain competitive.

Conclusion: 6 Difference Between a Traditional and Online Bank

6 Difference Between a Traditional and Online Bank: The choice between a traditional and online bank ultimately depends on an individual’s specific financial needs, preferences, and comfort level with technology. Traditional banks offer the convenience of physical branches, personalized service, and a wider range of products and services, while online banks provide cost savings, accessibility, and technological innovation. Some consumers may prefer a hybrid approach, utilizing both traditional and online banking services to meet their diverse financial requirements. Regardless of the choice, it’s essential to carefully evaluate the features, fees, security measures, and customer support offered by each banking model to make an informed decision that aligns with your financial goals and lifestyle.